Prime Day 2026 ran June 23–26. Ahead of the event, Stackline surveyed 1,500 shoppers about what they planned to buy, how much they intended to spend, and which tools they expected to use. Once the event closed, Stackline went back to the same population to measure what actually happened.

The post-event data confirms some of that intent and adds new texture to the rest. Here is what shoppers told us, and what it means for brands heading into the back half of the year.

Shoppers didn't stay on one platform

84% of shoppers browsed Amazon's Prime Day event, consistent with last year. But nearly half also browsed Walmart's Summer Deals Event (46%), and more than a third checked Target's Circle Deal Days (37%). Best Buy ran a competing Summer Tech Fest promotion alongside the three larger retailers, drawing a smaller but notable 5% of shoppers. Only 6% said they didn't browse any retailer's sale during the week.

The cross-shopping behavior shoppers said they would engage in before the event held up after it. Two-thirds of shoppers checked competing retailers, and Walmart grew its share of browsers year over year, up from 43% to 46%. Target held roughly steady, down slightly to 37% from 43%.

For brands selling across multiple retailers, that means pricing and content consistency matter as much during the event as before it. A shopper who finds a better deal or a clearer product page at a second retailer converts there instead, and that's still a win, just not the one brands necessarily planned for.

Category interest shifted by retailer, not just by event

Apparel led browsing across the board at 57%, a six-point increase over last year. Beauty followed at 43%, with household supplies, grocery, and electronics each landing in the mid-30s.

But the category mix looked different depending on where shoppers were browsing. Target shoppers over-indexed on beauty (52%) and grocery (45%) relative to Amazon. Walmart shoppers leaned into grocery (45%) and electronics (41%) more than Amazon shoppers did. Apparel was the top category everywhere, but the retailer a shopper chose said something real about what they were there to buy.

That distinction matters for how brands plan category-level messaging. A beauty brand selling on Target should expect a more receptive audience there than the topline Prime Day numbers alone would suggest. The same logic applies in reverse for grocery and electronics brands at Walmart.

Deal satisfaction followed a similar but not identical pattern. Looking at raw share of shoppers, apparel again led at 35%, with electronics at 27% and beauty at 26%. But the more telling number is relative: among shoppers who browsed each category, 76% of electronics shoppers felt they got the best promotions, nearly double grocery's 42% and nearly triple pet's 28%. With most shoppers coming into the event planning to stock up on basics, the everyday categories they showed up for most often were the ones that underdelivered against expectations once they got there.

Stocking up beat every other reason to shop

49% of shoppers said their primary motivation was stocking up on basics, up from 40% in pre-event intent data, the biggest gain of any motivation. One of the more surprising shifts was general browsing, which dropped from 33% before the event to 18% after. Shoppers who thought they'd show up to browse ended up showing up to buy.

This is consistent with what shoppers told Stackline before the event: Prime Day is a restocking moment first. What's new is how that motivation varied by retailer. Target shoppers were notably more likely to cite early holiday shopping (22%) and back-to-school (20%) as reasons to shop than Amazon shoppers were. For brands selling seasonal or school-adjacent categories, Target's shopper base is already thinking several months ahead, even during a summer event.

The takeaway for brands is straightforward: messaging that leads with value and everyday utility, rather than gifting or occasion-based framing, reaches the largest and most motivated share of shoppers. And for the browsing audience that showed up with less conviction, they converted anyway, which says a lot about what strong deals can do.

Deals improved, and shoppers noticed

23% of shoppers said deals were somewhat better than last year, and 10% said much better. The share who rated deals as worse dropped from 17% in 2025 to 14% this year. The majority, 53%, said deals were about the same.

That's a real improvement in sentiment, and it tracks with the better consumer confidence Stackline measured heading into the event. But the retailer-level breakdown surfaces one outlier worth flagging. Only 37% of Best Buy shoppers said deals were about the same as last year, the lowest share of any retailer, and Best Buy also drew the highest share of shoppers who said deals were worse.

Electronics shoppers tend to walk in with sharper price expectations, built from months of price tracking on big-ticket items, and that scrutiny shows up clearly in the sentiment data. For brands selling through Best Buy's promotional events, deal depth and visibility carry more weight with this audience than they do elsewhere.

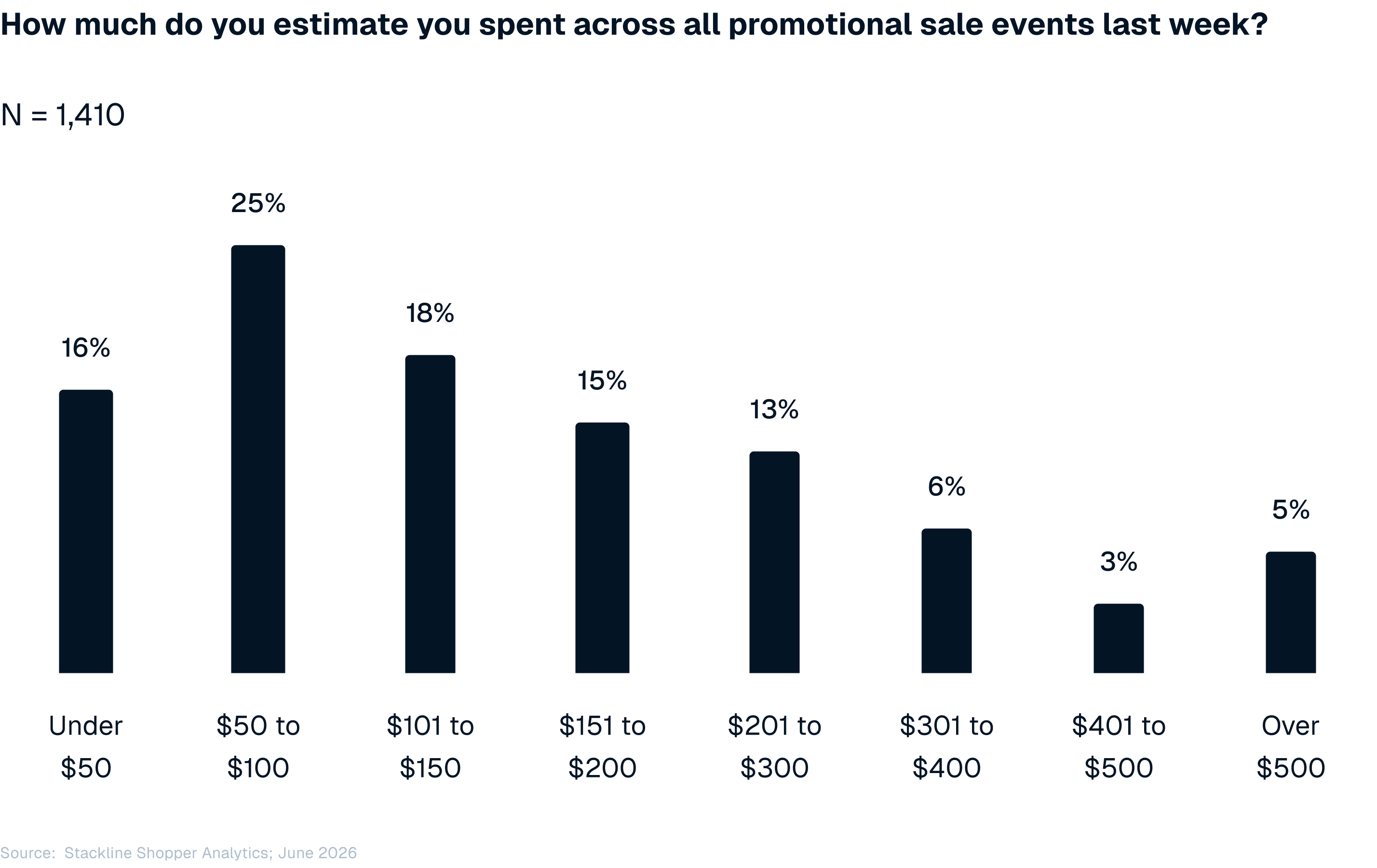

Most shoppers spent under $200, and stuck to their plans

The largest spending cohort, 25% of shoppers, spent between $50 and $100 across all promotional events during the week. Another 18% spent $101–150, and roughly 14% spent over $300. Nearly half of shoppers, 47%, said they spent about what they planned going in, and only 17% came in under budget.

37% spent more than they planned, which lines up with the lighter budget constraints shoppers described before the event: a third entered the week with no spending ceiling at all. But the overspend wasn't evenly distributed.

52% of Best Buy shoppers spent more than they planned, compared to roughly 37% across Amazon, Walmart, and Target. That tracks with one of the clearest motivations shoppers named overall: 28% said buying a higher-priced item now that it's on sale was a primary reason to shop. For a shopper eyeing electronics, a steep enough discount on the better TV or the upgraded model can make trading up feel like the smarter buy, not an indulgence.

For brands in high-ticket categories, that's a real opening: a deal deep enough to make the premium tier feel attainable can move shoppers up the line, not just across it.

Sale prices drove the vast majority of purchases

62% of shoppers said they only bought items that were on sale. Another 29% mixed full-price and sale purchases, and only 4% bought exclusively at full price.

A discount remains the dominant factor behind nearly every Prime Day purchase, which reinforces what the pre-event data already pointed to. Deal visibility, not just deal depth, continues to be the lever that converts browsing into purchases.

More than one in three shoppers used AI, and the tools they used are shifting

58% of shoppers said before the event that they planned to or were considering using AI to shop. 36% actually did. That gap between stated intent and real usage is sizable, but it points to room to grow rather than a shortfall: AI-assisted shopping is still early in its adoption curve, and the audience already primed to use it is large.

Among shoppers who used AI, the use cases were practical. Comparing prices led at 56%, followed by checking price history (42%), comparing products across retailers (29%), summarizing reviews (23%), and general product research (23%). This lines up closely with what Stackline found before the event, when price comparison was also the dominant use case. Shoppers are using AI to validate decisions, not to discover products from scratch.

The platform mix is where the real movement is. ChatGPT led overall usage at 14%, but Amazon's Alexa for Shopping came in close behind at 13%, a meaningful gain since BFCM last year. Google Gemini captured 11%. Before the event, Stackline found that 50% of shoppers had already tried Alexa for Shopping in some form, so this growth in active usage during a major event isn't a surprise, it's the natural next step in an adoption curve that was already underway.

Among the 13% of shoppers who used Alexa for Shopping specifically, the behavior was substantive. 46% viewed price history, 37% selected search results to compare, and a third reviewed AI-generated summaries directly in search results or on product pages. 32% went a step further and generated a personal shopping guide. That tracks with what Stackline found before the event: the most common Alexa behavior is asking questions directly in natural language, the same way shoppers interact with ChatGPT.

This convergence matters for product content strategy. As Stackline's PDP guide for a new era of shopping outlines, the brands best positioned to show up in AI-generated summaries and recommendations are the ones investing in structured, descriptive product content now, written to directly answer likely shopper questions rather than purely for keyword matching, not waiting until the next major event to start.

The signal for brands

The shopper who showed up for Prime Day 2026 wasn't waiting to be convinced. They had already compared prices, checked competing retailers, and in more than a third of cases, asked an AI tool to validate the decision before they made it. That's not a temporary posture brands need to plan around once a year. It's the baseline for every major sale event from here forward, and the brands that meet shoppers there are the ones building real momentum.

The categories and retailers that performed best did so by matching that posture: visible pricing, consistent content across channels, and deals that held up once shoppers actually compared. That same playbook, sharpened with what this event revealed, is exactly what positions brands to win even bigger at the next one.

The shoppers are already paying attention. The question is which brands will be ready to meet them.